Intercompany Overview

The Intercompany functionality allows you to record financial transactions that cover more than one company. Examples include

- a company records a voucher that includes expenses incurred by another group company

- a company pays a voucher that has been recorded in the general ledger of another company

- a company works and earns revenue on a project that is under the control of another group company

The system allows for individual accounts to be created to recognize the Debts owed by and to other group companies. The system also has subsidiary ledgers that record receivable and payable transactions between companies.

|

Note: If Intercompany accounts are always consolidated on financial reports, it is possible for a company to have Intercompany Receivable and Intercompany Payable accounts that will contain all transactions with other companies and use the subsidiary ledgers when details are needed. However, if Intercompany accounts are not always offset in consolidated statements, then it is recommended that a company have Intercompany Receivable and Intercompany Payable accounts for each group company. |

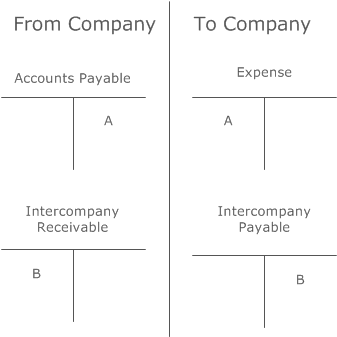

Intercompany Pairs is used to set up the intercompany receivable and payable accounts used to post financial documents that cross companies. These accounts are typically eliminated during company consolidation. For an example, see ![]() Intercompany Expense Example.

Intercompany Expense Example.

Additionally, this is used in situations where a company (working company)charges to a project that is owned by another company (owning company). These accounts recognize the revenue earned by the working company in the general ledger of the owning company. For an example, see ![]() Intercompany Revenue Example.

Intercompany Revenue Example.

|

Note: To recognize the revenue in the working company's general ledger, the revenue accounts from the project posting group are used. For more information, see Project Posting Group. |